Microsoft Dynamics 365 Finance and Operations (D365 F&O) operates on a continuous update model, releasing multiple major updates each year alongside regular quality and regulatory patches. For organizations running accounts payable on D365 F&O, this cadence represents both an opportunity and a governance challenge. Each update can alter workflow routing, approval logic, tax calculation behavior, payment processing rules, and integration touchpoints, often in ways that are not immediately visible in a test environment without deliberate, structured validation.

The accounts payable function sits at the intersection of financial accuracy, vendor relationships, cash management, and regulatory compliance. A disruption to AP workflows does not stay contained to the finance team. It cascades into payment runs, supplier trust, audit readiness, and month-end close timelines. For CIOs, CFOs, and compliance leaders, that exposure isn’t abstract, but translates directly into cost, reputational risk, and in regulated environments, potential liability.

Thoroughly testing AP workflows before every D365 F&O update isn’t a technical checkbox, but a governance discipline, and one that carries measurable consequences when it is treated as optional.

Key Takeaways

- AP workflows in D365 F&O are directly affected by update changes to matching logic, approval routing, tax calculations, and payment processing, all of which require validated regression testing before go-live.

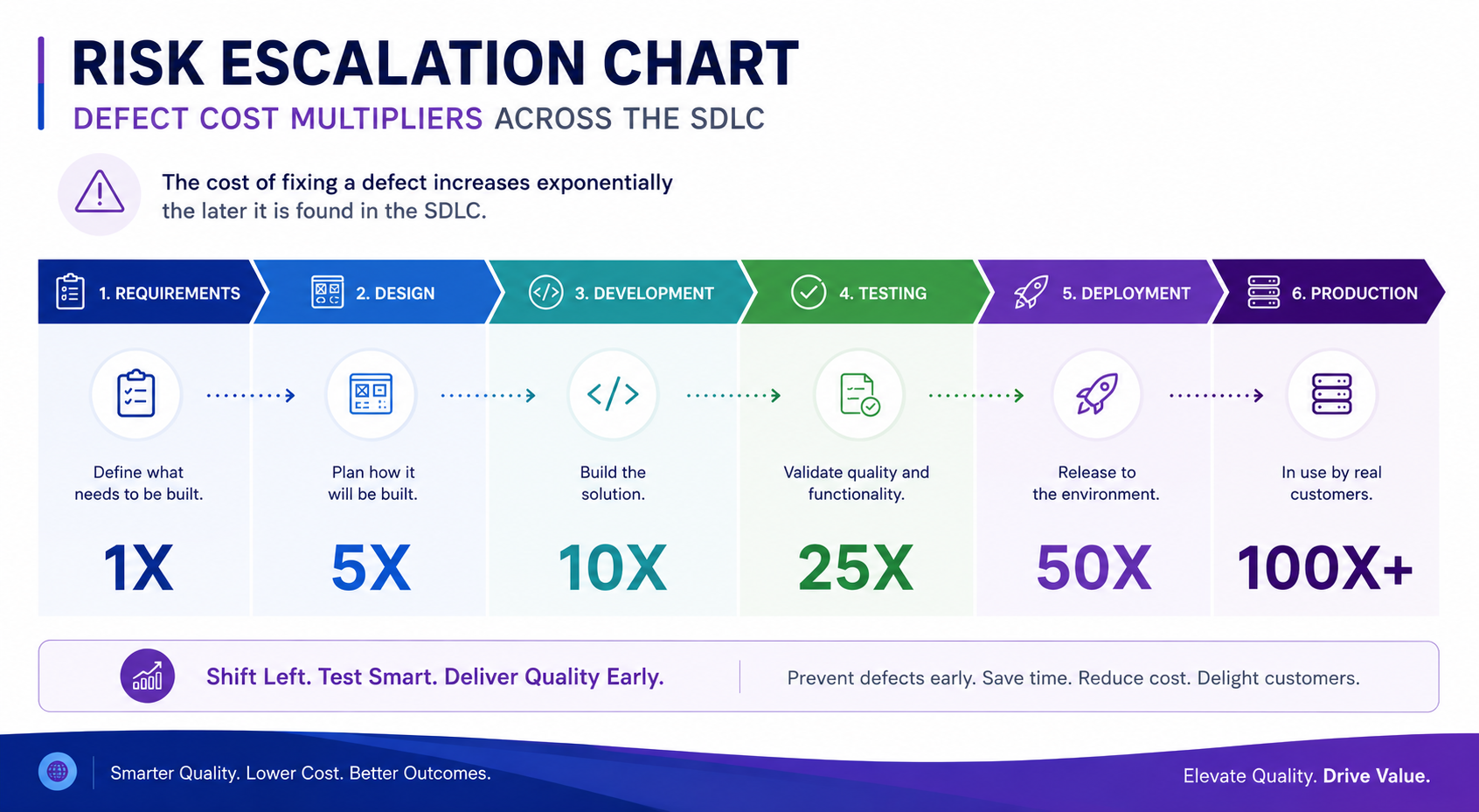

- Defects that reach production are significantly more expensive to remediate than defects caught during pre-update testing, both in direct remediation cost and in downstream operational disruption.

- Structured, repeatable test automation enables finance and AP teams to run comprehensive regression cycles within D365 F&O’s update cadence without scaling headcount or increasing test cycle time.

Why AP Workflows Are Particularly Vulnerable During D365 F&O Updates

Accounts payable in D365 F&O isn’t a single workflow, but a layered set of interdependent processes: purchase order matching, invoice registration and approval, payment proposal generation, vendor settlement, and outbound payment file creation. Each layer interacts with others, and each can be affected by update changes to underlying modules, including General Ledger, Tax, Procurement and Sourcing, and Cash and Bank Management.

Microsoft’s update releases regularly include changes to matching tolerances, workflow parameter defaults, tax engine logic, and payment format configurations. Organizations that do not run structured AP workflow testing before applying an update to production are effectively discovering any breaks in these processes after the fact, during live payment runs or month-end reconciliation.

The risk is compounded by the fact that many AP teams carry institutional knowledge in their people rather than in documented, repeatable test cases. When a D365 F&O update goes to production without systematic testing, there is no consistent baseline against which to measure what has changed.

The Cost Equation: Why Pre-Update Testing Pays for Itself

The financial argument for pre-update AP workflow testing is not difficult to construct. Research from IBM’s Systems Sciences Institute, a finding that remains one of the most consistently cited benchmarks in enterprise software quality management, established that defects identified and resolved in production cost between 15 and 30 times more to remediate than defects caught during the testing phase. While this figure originates from earlier software development research, its underlying logic has only become more relevant in the context of integrated, process-driven ERP systems where a single defect can propagate across connected workflows.

The cost difference is not simply a matter of developer time. In an AP context, a defect that reaches production can mean duplicate payments, missed payment runs, vendor statements that don’t reconcile, incorrect tax postings, and audit exceptions. Each of those consequences carries its own remediation effort, and in some cases, financial penalties.

Beyond direct remediation, there’s the operational downtime exposure. According to 2024 research from EMA Research, unplanned IT downtime now averages more than $14,000 per minute for enterprise organizations. For organizations where AP runs on D365 F&O and an update introduces a production defect that halts payment processing, even a contained outage of two to three hours carries a seven-figure exposure in lost productivity and recovery cost alone, before accounting for any vendor or regulatory consequences.

What the Data Shows About AP Workflow Error Risk

The accounts payable process is inherently sensitive to data integrity and workflow configuration. Research from the Institute of Finance and Management (IOFM) indicates that manual invoice processing carries an error rate of approximately 2%, and that this rate falls to below 0.8% in well-automated, validation-controlled environments. While this benchmark applies to processing operations rather than ERP update scenarios specifically, it illustrates a foundational principle: AP workflows are sensitive to configuration integrity, and that sensitivity does not diminish during a system update. It increases.

When a D365 F&O update changes matching parameters, payment terms defaults, or approval workflow routing, the behavioral delta between pre-update and post-update processing can introduce errors that look identical to manual processing errors, but are systemic and will repeat across every transaction until identified and corrected.

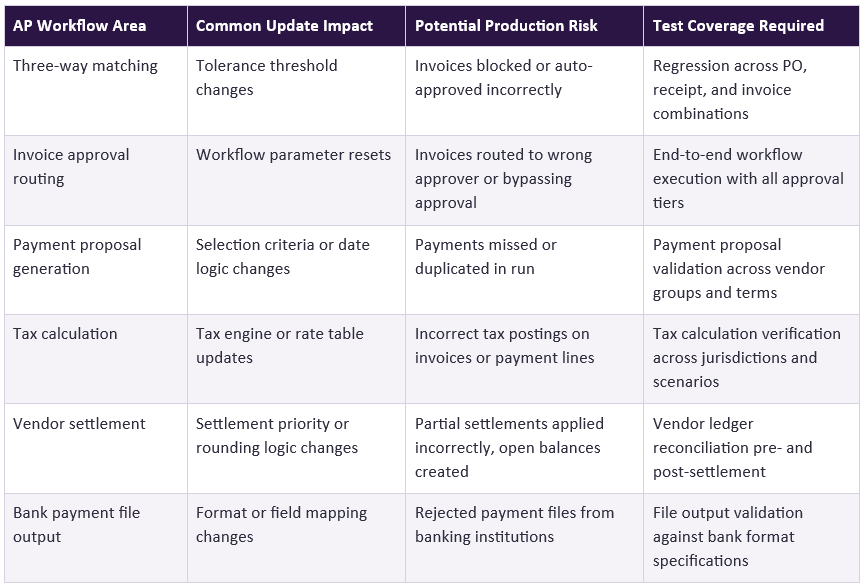

The following table outlines the primary AP workflow areas affected by D365 F&O updates, the nature of the risk each carries, and the corresponding test coverage required:

Governance Expectations Have Raised the Bar on Pre-Update Validation

Finance and compliance leaders increasingly treat ERP update validation as a governance requirement, not a technical precaution. For organizations subject to SOX, IFRS, or local regulatory financial reporting requirements, an untested D365 F&O update that introduces errors in AP posting or payment behavior isn’t a minor operational issue, but a controls failure.

External auditors and internal audit functions are becoming more specific in their expectations around ERP change management. Organizations are being asked to demonstrate that they have a systematic process for validating system changes that affect financial workflows, and that this process is documented and repeatable. Ad hoc, spreadsheet-based, or manually intensive testing approaches are increasingly difficult to defend in this context, because they are neither comprehensive nor auditable.

For compliance-focused teams, the governance case for structured AP workflow testing before D365 F&O updates is straightforward: the controls environment does not pause during an update window, and the organization’s ability to demonstrate control integrity depends on the quality of the change validation process.

Practical Principles for Structuring AP Workflow Test Coverage

Organizations that manage D365 F&O updates effectively tend to share several common practices in how they approach AP workflow testing. These aren’t aspirational standards, but operational disciplines that distinguish organizations with low update-related incident rates from those that regularly encounter post-update disruptions:

- Test case ownership sits with the AP team, not IT. Finance and AP users who understand the business intent of each workflow are better positioned to validate that a workflow behaves correctly after an update than technical testers who can confirm that a process executes but may not recognize when its output is wrong.

- Regressioncoverage is defined against live process variations, not just the baseline happy path. AP workflows carry significant scenario variability, including partial receipts, multi-currency invoices, prepayments, credit notes, and cross-entity transactions, all of which need to be represented in the test set.

- Testcycles are aligned to the update calendar, not to resourcing availability. D365 F&O operates on a fixed update schedule. Organizations that treat testing as a capacity-dependent activity, running what they can manage within available bandwidth, are consistently behind the update cycle and accepting unvalidated risk into production.

- Test results are documented as part of the change management record. Audit-ready evidence of pre-update testing is increasingly expected by both internal and external audit functions. Test results that exist only in a team member’s memory or informal email chains do not satisfy this expectation.

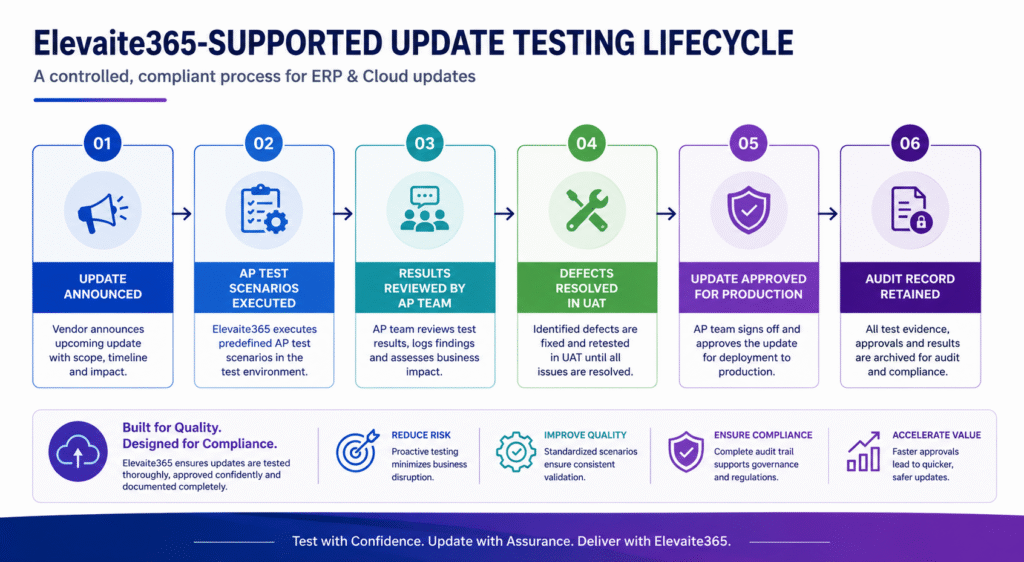

How Structured Test Automation Addresses the AP Testing Challenge

The core operational challenge in AP workflow testing is one of scale and consistency. The number of test scenarios required for comprehensive AP regression coverage, across matching rules, approval paths, payment types, tax scenarios, and vendor configurations, typically exceeds what finance teams can execute manually within an update window without disrupting their normal workload.

Elevaite365 Test Automation is built specifically for Microsoft Dynamics 365 environments and is designed to allow AP and finance users to execute structured, repeatable test automation without requiring technical development skills. This means that the team members who understand AP workflows best, finance leads, AP managers, and process owners, can take direct ownership of regression testing rather than translating requirements through an IT intermediary.

For organizations currently running Microsoft’s Regression Suite Automation Tool (RSAT) on D365 F&O, this transition does not require rebuilding existing test scripts from scratch. RSAT scripts can be converted directly into the platform, preserving the AP test coverage finance teams have already invested in while removing RSAT’s structural constraints around test self-healing and parallel execution.

For companies managing D365 F&O updates across multiple legal entities, integrations, or complex AP configurations, this capability reduces the time and resource commitment required to achieve comprehensive pre-update test coverage. It also creates an auditable record of test execution and results that supports governance and compliance reporting requirements.

The goal of structured test automation in this context isn’t to eliminate human judgment from the AP testing process, but to reduce the manual effort required to run coverage at scale, so that human judgment can focus on interpreting results and making go/no-go decisions with confidence rather than being consumed by test execution.

Conclusion: Pre-Update AP Testing as a Financial Governance Discipline

The decision to thoroughly test AP workflows before a D365 F&O update is ultimately a risk management decision. The cost of discovering an AP workflow defect in production, in remediation time, payment disruption, audit exposure, and vendor relationship impact, consistently exceeds the cost of structured pre-update testing by a significant margin. The governance environment for finance organizations is reinforcing this calculation, as auditors and compliance functions raise expectations around ERP change management controls.

Organizations that treat pre-update AP workflow testing as a governance discipline, with defined coverage, AP team ownership, and documented results, are better positioned to absorb the pace of D365 F&O updates without accumulating unvalidated risk in their financial systems. The tools and approaches to make this practical at scale exist. The question for most organizations is whether their current testing process is structured enough to keep pace with the update cadence they are already managing.

Frequently Asked Questions

What AP workflows in D365 F&O are most affected by updates?

The workflows most consistently affected by D365 F&O updates include three-way matching, invoice approval routing, payment proposal generation, tax calculation, and vendor settlement logic. These areas are particularly sensitive because they interact with multiple modules and are directly tied to financial posting accuracy.

Updates to the Tax module or Procurement and Sourcing parameters, in particular, can change AP workflow behavior without being explicitly called out as AP changes in the update release notes. This is why regression testing against live AP scenarios is more reliable than relying on release note review alone to determine whether a given update requires AP-specific validation.

How often does Microsoft release updates that can affect AP workflows?

Microsoft releases major D365 F&O updates on a regular cadence, typically two to four times per year for proactive quality updates and continuous updates, with additional service updates applied more frequently. Not every update will materially change AP workflow behavior, but organizations cannot reliably determine which updates have AP impact without running structured validation.

This is one of the central governance challenges of operating D365 F&O at an enterprise level. The update frequency is an asset from a product capability perspective, but it creates a continuous testing obligation that manual-only approaches struggle to keep pace with without either accepting coverage gaps or significantly increasing testing resource commitment.

What is the difference between user acceptance testing and AP regression testing in this context?

User acceptance testing (UAT) is typically designed to validate new functionality or configuration changes introduced deliberately as part of a project or update. AP regression testing serves a different purpose: it validates that existing, working AP processes continue to behave correctly after a system change that was not specifically designed to alter them.

In D365 F&O update scenarios, regression testing is often more critical than UAT because the risk isn’t in the intentional changes, but in the unintended side effects. An organization that runs robust UAT on new features but skips regression on existing AP processes is testing the least risky part of the update while leaving the highest-risk area unvalidated.

How long should AP workflow testing take before a D365 F&O update?

The appropriate test cycle duration depends on the complexity of the AP configuration, including the number of legal entities, vendor groups, payment methods, tax jurisdictions, and integration touchpoints. For organizations with moderate AP complexity, a structured regression cycle covering the key workflow areas can typically be completed in two to five business days with the right test automation tooling in place.

Without automation, the same coverage often requires two to four weeks of manual effort, a timeline that frequently does not fit within the available window between an update’s sandbox availability and its mandatory production application date. This is one of the primary drivers of test coverage compromise in manual-only AP testing approaches.

What documentation should organizations retain from pre-update AP testing?

At a minimum, organizations should retain a record of which test scenarios were executed, the date of execution, the update version being validated, the test results for each scenario, and evidence of any defects raised and resolved prior to production go-live. This documentation serves both internal change management purposes and external audit requirements.

For organizations subject to SOX or equivalent financial reporting controls, the ability to demonstrate that material financial workflows were validated before a system change was applied to production is increasingly treated as a control in its own right. Test documentation that is structured, dated, and tied to specific workflow scenarios provides a defensible audit trail, while informal or undocumented testing provides none.

A note on statistics used in this article:

- The defect cost multiplier (15–30x for production versus testing phase) is sourced from IBM’s Systems Sciences Institute. While this research originates from earlier software development contexts, it remains one of the most consistently cited benchmarks in enterprise software quality management and its underlying logic has become more relevant in integrated ERP environments.

- The unplanned IT downtime cost figure (more than $14,000 per minute for enterprise organizations) is sourced from 2024 research by EMA Research (Enterprise Management Associates).

- The manual invoice processing error rate (~2%, falling to below 0.8% in automated environments) is sourced from research by the Institute of Finance and Management (IOFM).