Accounts receivable is one of the most cash-sensitive functions in any enterprise. It governs how quickly revenue converts to liquidity, how accurately customer balances are maintained, and how reliably the organization can close its books and meet reporting obligations. For organizations running AR on Microsoft Dynamics 365 Finance and Operations (D365 F&O), the platform’s continuous update model introduces a recurring and underappreciated risk: each update has the potential to alter the behavior of AR workflows in ways that, if undetected before go-live, translate directly into billing errors, collection delays, revenue recognition issues, and audit exposure.

The D365 F&O update cadence is not optional. Microsoft releases major updates on a fixed schedule, and organizations are required to apply them within defined windows. For AR teams, this creates a compliance-adjacent testing obligation that sits alongside, and sometimes competes with, the operational demands of day-to-day collections, invoicing, and reconciliation. When that testing is incomplete or informal, the risk does not disappear. It transfers into production, where the cost and complexity of remediation are significantly higher.

Understanding which AR workflows carry the greatest update risk, and why, is the foundation of a defensible pre-update governance process. For finance, operations, and audit leaders, that understanding directly informs how testing resources are allocated, how go-live decisions are made, and how the organization demonstrates control integrity to internal and external audit functions.

Key Takeaways

- D365 F&O updates regularly affect AR-critical areas including customer invoicing, collection workflows, revenue recognition parameters, and integration touchpoints with banking and tax systems, all of which require structured regression validation before production go-live.

- AR workflow disruptions caused by untested updates carry compounding financial consequences, including extended DSO, disputed invoices, delayed cash collection, and weakened audit trails.

- Organizationswith standardized, repeatable AR testing processes are materially better positioned to absorb the D365 F&O update cadence without accumulating unvalidated risk in their revenue cycle.

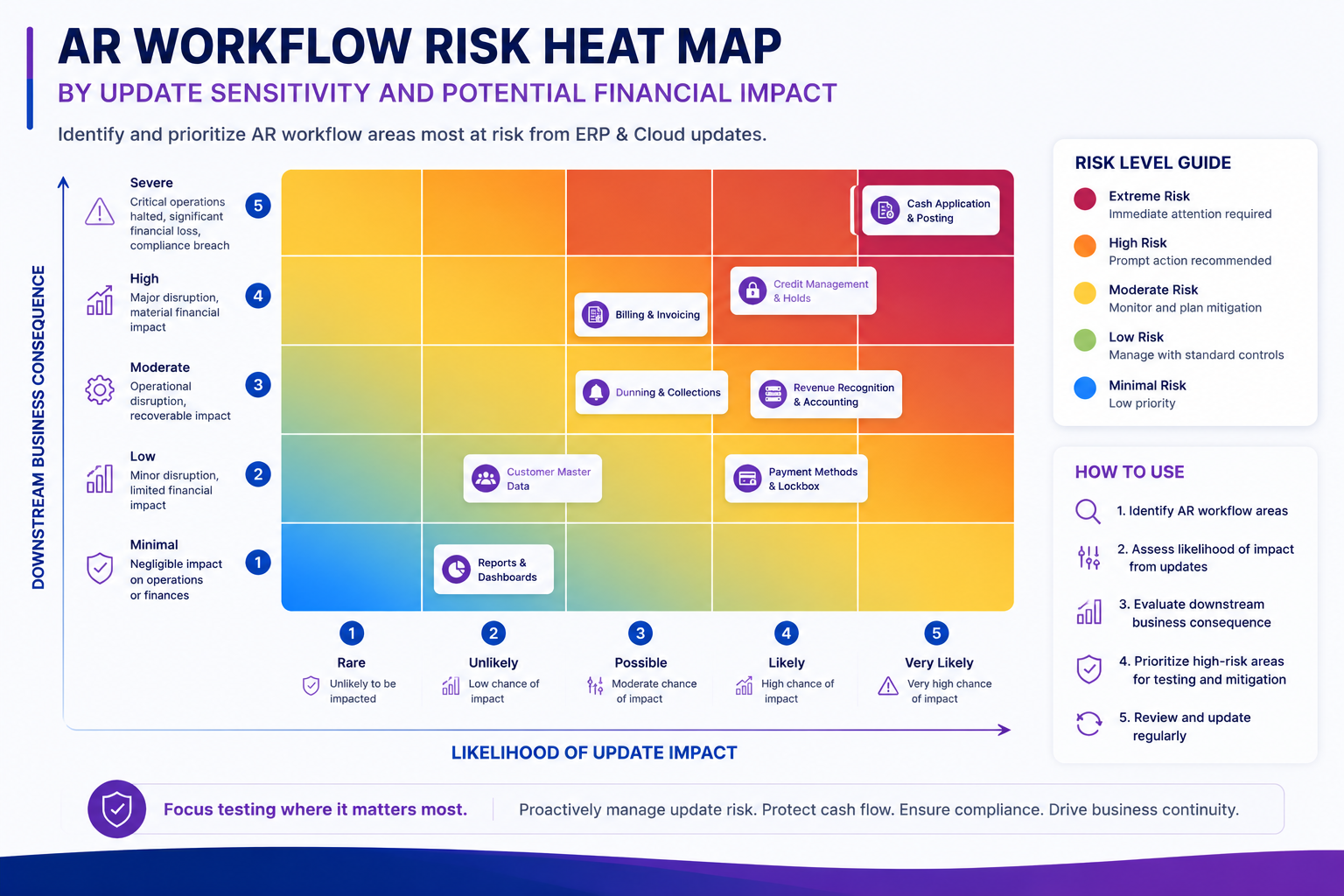

Which AR Workflows Are Most Exposed During a D365 F&O Update

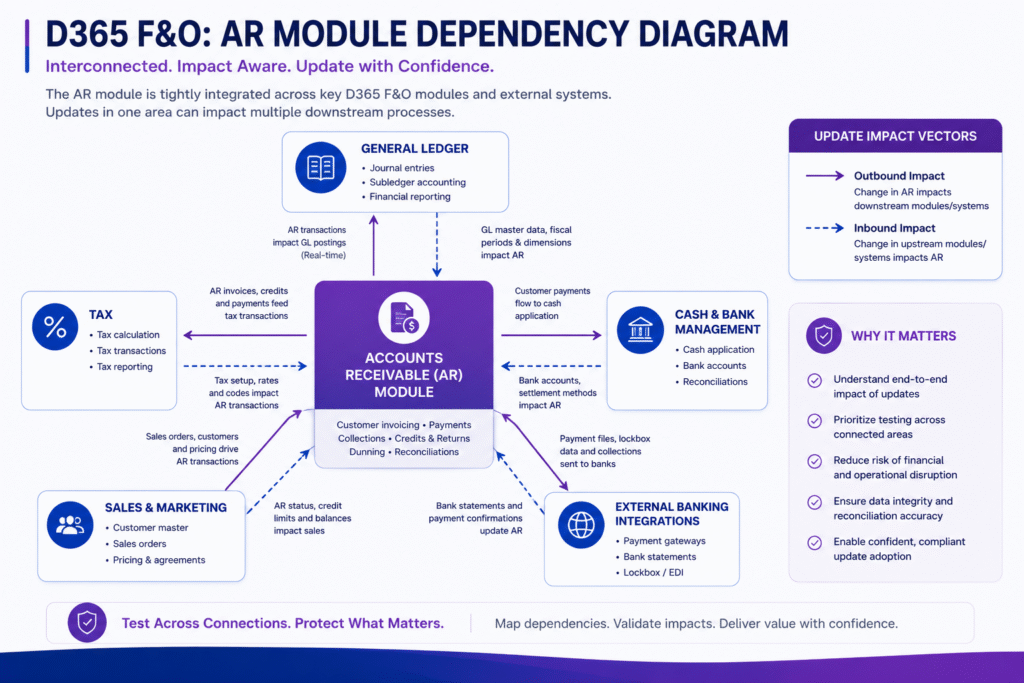

Accounts receivable in D365 F&O isn’t a single module, but a network of interdependent processes spanning customer master data, invoicing, credit management, collections, cash application, and revenue posting. Updates to adjacent modules, including General Ledger, Tax, Sales and Marketing, and Cash and Bank Management, can alter AR behavior without being explicitly flagged as AR changes in Microsoft’s release notes.

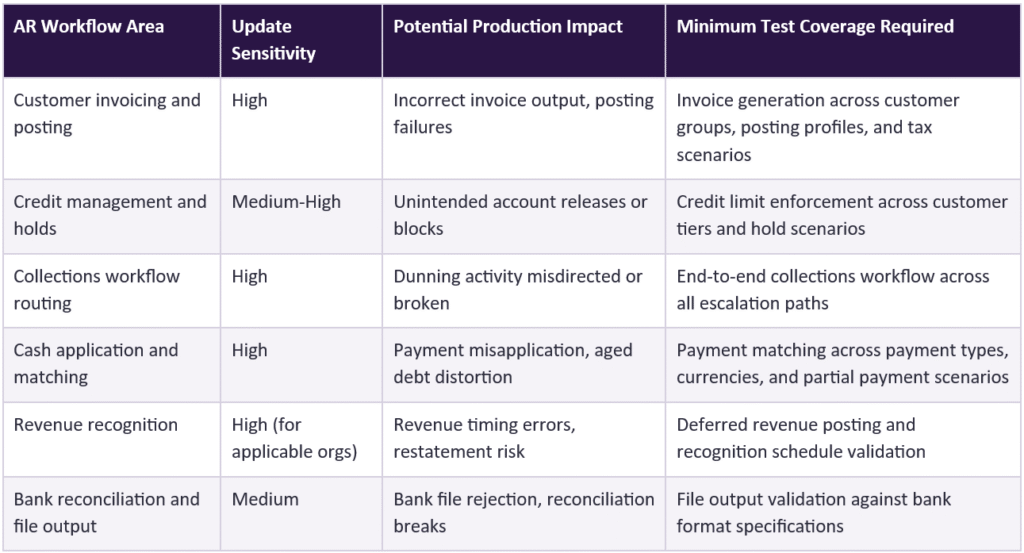

The AR workflows that carry the highest update sensitivity include:

- Customer invoicing logic and posting profiles, where changes to number sequences, posting rules, or transaction types can produce incorrect invoice outputs or posting failures

- Credit limit management and hold logic, where parameter changes can inadvertently release or block customer accounts outside of intended policy

- Collections workflow routing, where update-related resets to workflow parameters can redirect dunning activities to incorrect queues or break automated escalation paths

- Cash application and bank reconciliation, where changes to matching algorithms or bank format configurations can cause payment misapplication or file rejection

- Revenue recognition scheduling, where updates touching deferred revenue or multi-element arrangement logic can alter the timing of revenue posting in ways that affect financial reporting

Each of these areas is operationally critical, and each can fail silently in a test environment if the testing approach doesn’t cover the specific scenario combinations that appear in live AR processing.

The Financial Consequence of Untested AR Workflow Failures

When an AR workflow defect reaches production following a D365 F&O update, the downstream consequences are rarely contained to a single transaction. Invoicing errors can trigger customer disputes, which pause payment collection and extend Days Sales Outstanding. Cash application failures cause aged debt balances to misrepresent the true receivables position. Revenue recognition errors may require restatement or audit explanation.

The financial sensitivity of AR to process configuration is well established in independent research. According to The Hackett Group’s research on customer-to-cash process management, organizations that integrate early collections outreach and real-time credit risk assessment into their AR workflows reduce average delinquency by 8.4 days and improve DSO materially. The implication for D365 F&O update management is direct: if an untested update disrupts the configuration that enables these disciplines, the financial benefit evaporates, and in many cases the organization will not identify the source of the degradation until the next collections review.

The governance exposure is equally significant. A 2025 Shared Services and Outsourcing Network global report, cited by Auxis in their March 2025 analysis of AR best practices, found that standardized, centralized AR processes reduced DSO by three days, improved dispute resolution by 59%, and cut aged debt by 75%. These gains are built on stable, correctly configured process logic. A D365 F&O update that alters collections routing, customer hold parameters, or payment matching behavior without prior validation can undermine this configuration systematically and at scale.

Why AR Testing Is Harder Than It Appears

One of the persistent challenges of AR regression testing in D365 F&O is the breadth of scenario coverage required to achieve meaningful assurance. AR processes in enterprise deployments carry significant variability: multi-currency invoicing, intercompany transactions, partial payments, credit note applications, prepayment handling, customer-specific payment terms, and complex revenue recognition arrangements all behave differently and all need to be represented in the test set.

Organizations that approach AR update testing with a simplified “happy path” script, validating only the most common invoice-to-payment scenario, are testing a narrow slice of live AR behavior. The defects most likely to reach production aren’t in the scenarios that are always tested, but in the edge cases and configuration combinations that are tested inconsistently or not at all.

This testing gap is compounded by the operational reality that AR teams are running parallel to their testing obligation. Collections cycles, customer disputes, cash application backlogs, and month-end close pressures don’t pause during a D365 F&O update window. The result is that testing is frequently completed under time pressure, with coverage determined by what the team can manage rather than what the risk profile of the update requires.

The following table maps the primary AR workflow areas against their D365 F&O update sensitivity and the corresponding testing requirement:

The Operational Disruption Profile of ERP Updates

The risk of operational disruption from an untested ERP update is not hypothetical. Independent research consistently documents the scale of disruption that inadequate pre-go-live validation introduces. According to data summarized from Gartner and Panorama Consulting Group findings compiled by RubinBrown, 51% of companies experience operational disruptions when going live with a new ERP system or update. While this figure spans all ERP go-live types, it reflects the systemic testing and validation gaps that affect organizations at scale, including those applying mandatory D365 F&O updates to live AR environments.

For finance leaders, the relevant question isn’t whether ERP updates carry disruption risk in the abstract, but whether the organization’s current AR testing process is structured well enough to identify the specific defects that would affect collections, invoicing, and cash application before they reach production. The answer to that question determines whether a D365 F&O update becomes a controlled governance event or an unplanned remediation exercise.

What Auditors Now Expect From AR Update Validation

AR workflow validation has become an audit-defensible discipline in its own right. The driver isn’t IT preference but pressure from finance leadership, internal audit, and external auditors who increasingly treat ERP change events as moments where revenue recognition, customer invoicing, and cash application controls have to be re-verified. For organizations operating under SOX, IFRS 15, or sector-specific revenue rules, a D365 F&O update that quietly alters posting logic or matching behavior is the kind of finding auditors are now trained to look for.

What auditors are asking for has shifted in a measurable way. The question is less about whether validation happened and more about whether the organization can produce a structured record of which AR scenarios were tested, by whom, on which version of D365 F&O, and with what result. Informal testing, undocumented spot checks, and email-trail evidence are increasingly being treated as the absence of a control rather than imperfect documentation of one.

This raises a practical bar that AR teams have to meet. Test coverage in this environment can’t stop at technical execution; it also has to confirm business behavior: that invoices reflect the correct terms, that collections workflows behave according to current credit policy, that cash application produces ledger balances that reconcile to bank statements. The people best positioned to answer those questions are AR and finance professionals, not IT testers, which is what makes finance ownership of the test scenarios meaningful rather than nominal.

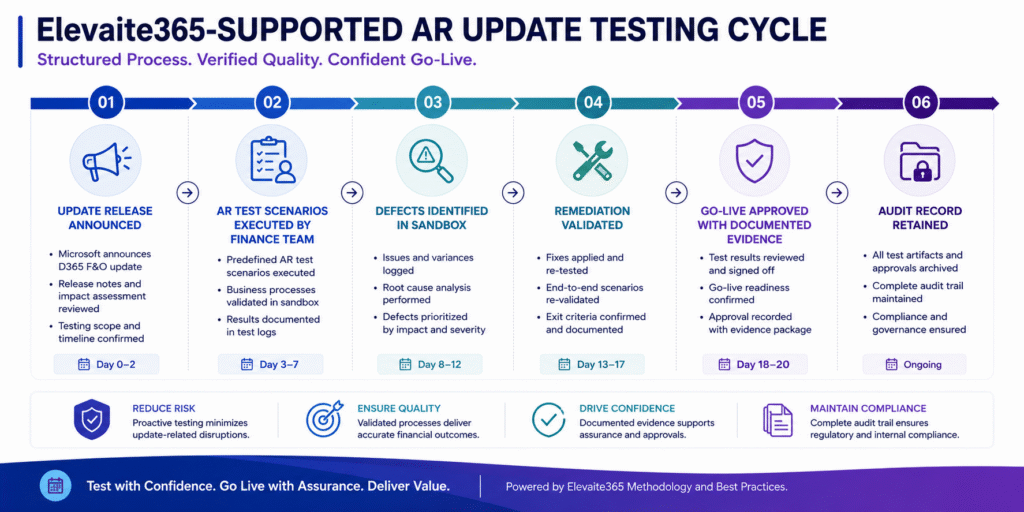

How Structured Test Automation Supports AR Update Governance

The practical constraint on AR update testing is one of capacity and consistency. Achieving comprehensive scenario coverage across all AR workflow areas, across all relevant customer configurations, payment types, and integration touchpoints, is beyond what most AR teams can execute manually within the update window without displacing operational priorities.

Elevaite365 Test Automation is purpose-built for Microsoft Dynamics 365 environments and enables AR and finance teams to execute structured, repeatable regression testing without requiring technical development skills. This means that the AR professionals who understand customer invoicing, collections policy, and cash application rules can take direct ownership of pre-update validation rather than depending on IT to interpret and execute those workflows on their behalf.

For organizations managing D365 F&O updates across complex AR configurations, including multiple legal entities, currencies, or revenue recognition arrangements, this capability allows comprehensive coverage to be achieved within the available update window. It also produces a structured, dated record of test execution and results that supports the governance and audit documentation requirements that finance leaders are increasingly expected to meet.

The licensing model also affects what is operationally feasible. Test platforms that price by execution count or that cap test script volume create a structural incentive to under-test, particularly in AR environments where comprehensive scenario coverage may require hundreds of runs across customer groups, currencies, and credit configurations. Platforms without per-execution or per-script ceilings remove that constraint, allowing finance teams to run the full regression suite overnight or across a weekend without trading depth of coverage against contract terms.

The goal isn’t to automate judgment out of the AR testing process, but to reduce the manual effort required to achieve coverage at scale, so that AR and finance leadership can make informed, evidence-based go-live decisions rather than accepting unvalidated risk into production under time pressure.

Conclusion: AR Update Risk Is a Finance Governance Responsibility

Accounts receivable risk in D365 F&O updates isn’t a testing problem owned by IT, but a finance governance responsibility that requires structured validation of the workflows on which revenue recognition, cash collection, and reporting accuracy depend. The consequences of inadequate pre-update testing in AR are measurable: extended DSO, invoice disputes, cash application errors, and audit exposure that can persist well beyond the update window in which they originate.

Organizations that treat pre-update AR workflow validation as a governance discipline, with defined coverage, AR team ownership, and documented results, are better positioned to absorb the pace of D365 F&O’s continuous update model without compromising the integrity of their revenue cycle. The tools and processes to make this practical at scale are available. The governance case for using them is clear. The remaining question is whether the current testing approach is matched to the complexity of the AR environment it is meant to protect.

Frequently Asked Questions

What accounts receivable workflows in D365 F&O are most likely to be affected by an update?

The AR workflows with the highest update sensitivity are customer invoicing and posting, collections routing, cash application and matching, credit limit management, and revenue recognition for organizations using deferred revenue or multi-element arrangements. These areas interact with multiple D365 F&O modules, making them vulnerable to indirect changes introduced by updates to General Ledger, Tax, or Cash and Bank Management.

The challenge is that update release notes do not always identify AR-specific behavioral changes, particularly when the change originates in an adjacent module. This is why regression testing against the full range of live AR scenarios provides more reliable assurance than release note review alone.

How can an untested D365 F&O update affect Days Sales Outstanding?

A D365 F&O update that disrupts collections workflow routing, customer hold logic, or dunning automation can delay outbound collection activity without any visible error message. The result is that invoices that should have triggered an automated follow-up do not, and DSO extends before the cause is identified.

The financial impact compounds over time. If the disruption affects a collections workflow that runs across an entire customer segment, the DSO impact isn’t limited to a single invoice but affects every account in that segment for the duration of the update cycle, a consequence that is difficult to reverse quickly and has direct implications for cash flow forecasting and working capital reporting.

What is the difference between AR regression testing and standard UAT in a D365 F&O update context?

User acceptance testing is designed to validate deliberate changes introduced by a project or update, confirming that new functionality or configuration works as intended. AR regression testing serves a different and often more critical purpose: it validates that existing, correctly functioning AR processes continue to behave correctly after a system change that was not designed to affect them.

In D365 F&O update scenarios, the greatest risk isn’t in the intentional changes, but in the unintended side effects on AR workflows that were working correctly before the update. An organization that focuses UAT effort on new features but skips regression testing on collections, cash application, and invoicing is leaving the highest-risk workflows unvalidated.

How should organizations document AR testing before a D365 F&O update to satisfy audit requirements?

At a minimum, audit-defensible pre-update AR testing documentation should include the specific test scenarios executed, the update version being validated, the date of test execution, the results of each scenario, and evidence of any defects raised and resolved before production go-live. This documentation should be linked to the change management record for the update.

For organizations subject to SOX or equivalent financial reporting controls, the ability to demonstrate that AR invoicing, revenue recognition, and cash application workflows were validated before a system change was applied to production is increasingly treated as a financial control in its own right. Informal or undocumented testing does not satisfy this expectation regardless of the quality of the testing itself.

How does the D365 F&O update schedule affect AR testing capacity planning?

Microsoft releases major D365 F&O updates on a fixed schedule, typically two to four times per year, with additional service updates applied more frequently. Each update opens a sandbox validation window before mandatory production application, and organizations that have not structured their AR testing for this cadence consistently find themselves compressed against the production deadline.

The practical consequence is that manual-only AR testing approaches either accept incomplete coverage or require significant temporary resource allocation to meet the update window. Test automation resolves this by enabling comprehensive AR scenario coverage to be executed within the available sandbox window without displacing operational AR priorities, making the D365 F&O update cadence manageable rather than a recurring constraint on governance quality.

A note on statistics used in this article:

- The Hackett Group 8.4-day delinquency reduction figure is sourced via Auxis’s March 2025 AR best practices analysis, which cites The Hackett Group’s Customer-to-Cash Receivables research directly. The Hackett Group is an independent, non-vendor research and advisory firm.

- The SSON 2025 DSO reduction, dispute resolution (59%), and aged debt (75%) statistics are sourced from the same Auxis March 2025 publication, which cites the SSON 2025 global shared services report directly.

- The 51% operational disruption figure is sourced from RubinBrown’s ERP statistics summary, which aggregates findings from Gartner and Panorama Consulting Group research.